Ever wondered why, even after years of working, many people still struggle with savings? They keep waiting for the “right time” to save, but the truth is—it never comes. The bills, EMIs, online shopping discounts, and weekend outings always take priority. What happens next? At the end of the month, the bank balance barely survives until the next salary.

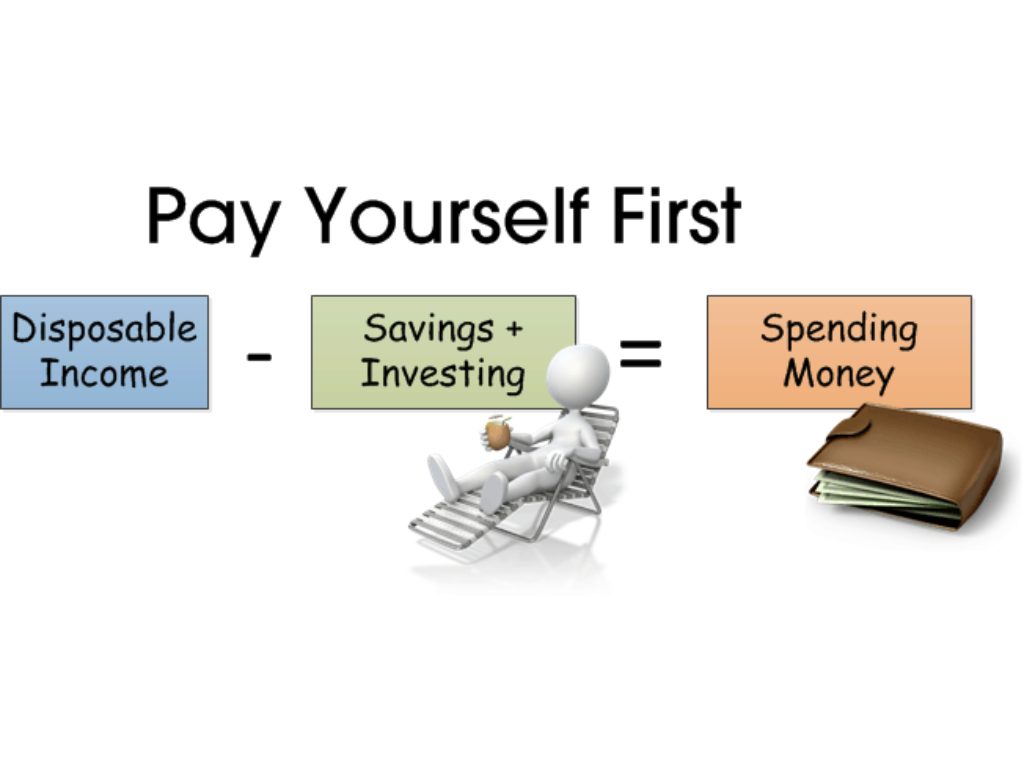

Here’s where the Pay Yourself First Rule comes in—a timeless principle of wealth-building. The idea is simple: before you pay your bills, rent, or even buy groceries, set aside a portion of your income for savings. By doing this, you ensure your financial future comes first, not last.

This rule is more than just a habit; it’s a mindset that transforms how you handle money.

Why Most People Struggle to Save

Let’s be honest—most of us wait until the end of the month to see “how much is left” to save. But in reality, almost nothing is ever left. Here are the common reasons why:

- Lifestyle inflation: The more you earn, the more you spend.

- Impulse buying: Discounts, sales, and instant online purchases eat away at income.

- Lack of planning: No fixed savings plan means savings take the last seat.

- Unexpected expenses: Medical bills, sudden repairs, or emergencies consume any extra cash.

The Pay Yourself First Rule flips this cycle upside down.

What Exactly Is the Pay Yourself First Rule?

The concept is straightforward: Treat your savings like your most important bill.

Every month, as soon as your salary hits your account:

- Move a fixed percentage (say 20%) into a savings account or investment.

- Forget that money exists—it’s not for shopping, not for dining out, not for splurging.

- Use the remaining amount for your monthly expenses.

This way, saving is no longer optional—it becomes automatic.

How to Apply the Rule in Your Life

1. Decide Your Savings Percentage

Start with 10–20% of your income. If that feels high, even 5% is better than nothing. Slowly increase the percentage as your income grows.

2. Automate Your Savings

- Set up an auto-debit from your salary account to a recurring deposit, mutual fund SIP, or PPF.

- The less you see, the less you’re tempted to spend.

3. Create Different Buckets

Don’t just “save” blindly. Divide your savings into goals:

- Emergency Fund

- Retirement Savings

- Investment for Growth

- Short-term Goals (vacation, gadgets, home appliances)

4. Cut Down on Non-Essential Spending

Track small daily expenses like coffees, snacks, or impulse shopping. Redirect those into your savings bucket.

5. Reward Yourself

Saving doesn’t mean sacrifice. Occasionally treat yourself, but only after you’ve paid yourself first.

Benefits of Paying Yourself First

1. Stress-free money management: No more worrying about whether you saved enough.

2. Faster financial growth: Consistency beats irregular large deposits.

3. Security in emergencies: Your savings will have your back.

4. Disciplined lifestyle: Teaches you to live within your means.

5. Wealth-building habit: Over time, your money works for you.

Quick Tips to Boost the Rule’s Impact

- Start small but stay consistent.

- Increase savings percentage with every raise.

- Keep a separate account for savings to avoid temptation.

- Track progress every 6 months.

- Invest wisely—don’t let money sit idle.

Conclusion

The Pay Yourself First Rule is one of the smartest money habits anyone can adopt. By simply saving a portion of income before spending, you set yourself on the path to financial independence and peace of mind. It’s not about how much you earn—it’s about how you manage what you have.

So, the next time your salary arrives, remember: your future deserves the first slice, not the leftovers.

#PersonalFinance #MoneyManagement #SavingsTips #FinancialFreedom #PayYourselfFirst

Editor’s Note: This article was originally published here: https://thelifetrackr.com/the-pay-yourself-first-rule-save-a-portion-of-income-before-spending/ by @Kairav and @krutika